An Analysis of Cryptocurrency Whale Trade Size and Direction

Where are whale trades made?

Key Insights:

- OKEx had the most number of whale trades, the largest average whale trade size, and the largest daily trade every day for the month of June.

- LMAX Digital had the highest average overall trade size (.69 BTC), nearly double that of the second highest ranked exchange Bitstamp (.37 BTX).

- Exchanges that had lower average trade sizes such as OKEx, Binance and Huobi, had higher average whale trade sizes, indicating that high-volume, more “retail-oriented” exchanges also have a significant user base of high-volume traders.

- BTC-USDT pairs had more whale trades than BTC-USD pairs.

Trade data can reveal rich insights about an exchange’s user base. In this report, we explore the trade size, direction and count of transactions on 11 exchanges.

Trader profiles in crypto markets can range from the smallest of retail traders to the largest of whales. Exchanges often cater for different trader profiles through targeted marketing and trading features in order to differentiate in the competitive exchange landscape. With this analysis, we found that each exchange has a unique composition of trades, at times unexpected.

While it is impossible to know the identity of the trader behind any given trade, we can use the trade size as a proxy for differentiating “whale” from “retail” traders.

Ultimately, this report seeks to explore the differences in exchange user bases, with a focus on large trades. In Part 1, we focus on exchange summary statistics and whale trade counts.

Methodology

We selected a range of exchanges that exhibit significant volume, yet encompass different user bases due to geography, active trading pairs, regulatory regime, and overall industry reputation.

We used trade data provided by Kaiko for the month of June 2020. We selected the highest volume BTC spot pair on 11 exchanges: BTC-USDT on Binance, BTC-USDT on Huobi, BTC-USD on Bitstamp, BTC-USD on Coinbase, BTC-USD on Bitfinex, BTC-USD on Kraken, BTC-JPY on Liquid, BTC-USDT on OKEx, BTC-JPY on Bitflyer, BTC-USD on LMAX Digital and BTC-USD on Gemini.

We define a whale trade as any trade ≥ 10 BTC.

Because the difference between “retail” exchanges and “institutional” exchanges is blurry, we tried not to focus this report along the lines of this classification, instead relying on the data to speak for itself. When we do refer to “retail” vs “institutional”, we looked at overall industry reputation and how exchanges market their trading services. [1]

[Edit 08/07 2020]: Additionally, this report assumes that trade data collected from these exchanges represents actual trades made. Many exchanges will break apart a large trade into many small trades if the order book does not have enough volume to support the trade size. Every exchange has a slightly different methodology for recording trade data, often unspecified, which poses a limitation to fully understanding the extent of large trades made on these exchanges.[2]

Exchange Summary Statistics

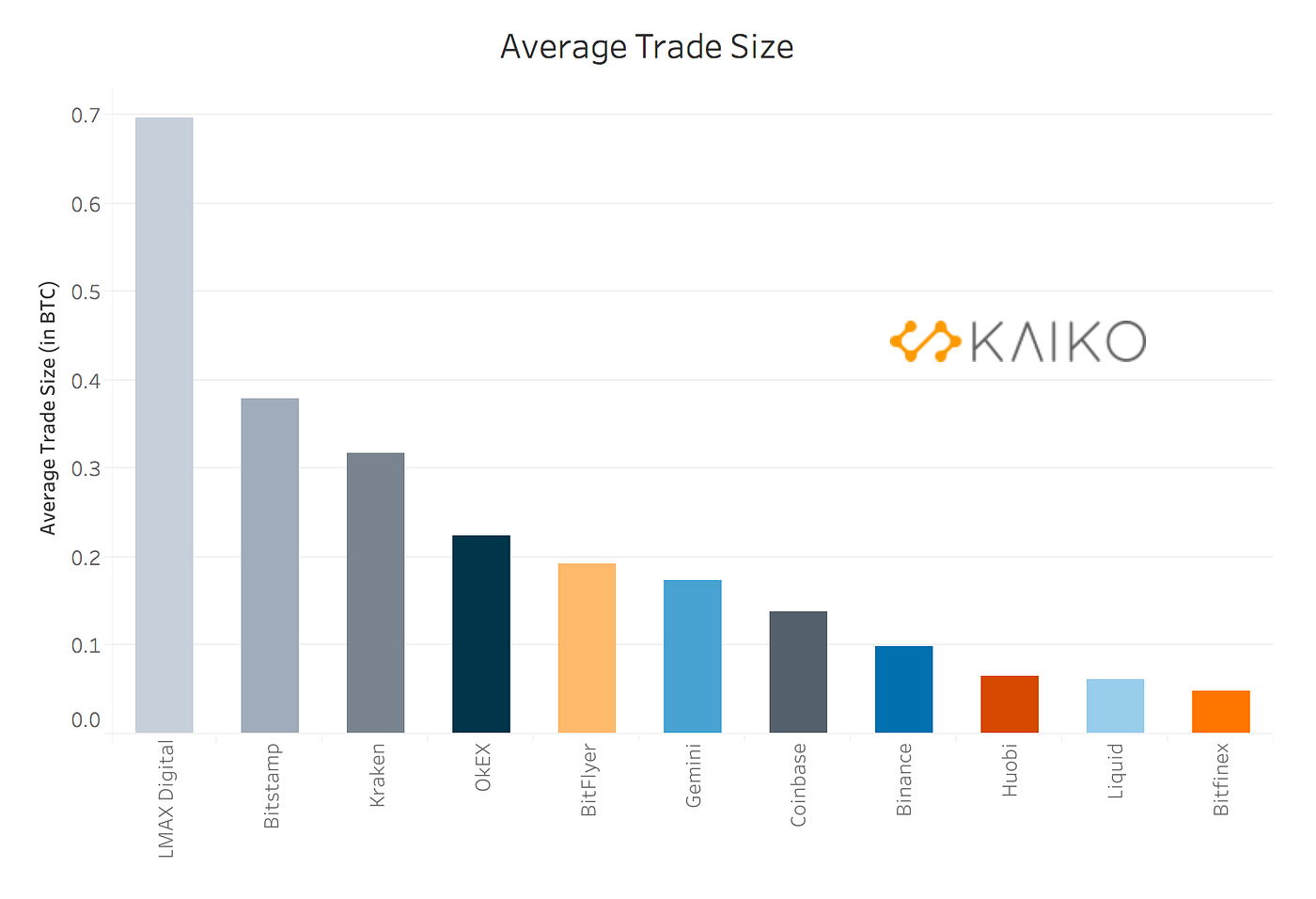

We first looked at the average trade size (in BTC) on the 11 exchanges we selected. We found that LMAX Digital had by far the highest average trade size at .6968 BTC, which is expected considering their targeted user base is almost entirely institutional. LMAX Digital’s average trade size was nearly double that of Bitstamp’s (.3783 BTC), the second ranked exchange. What was surprising was that Bitstamp’s average trade size was more than double that of its close competitors Gemini (.1739 BTC) and Coinbase (.1373 BTC).

As expected, more retail oriented exchanges such as Binance, Huobi, Liquid, and Bitfinex had lower average trade sizes, at .0997 BTC, .0653 BTC, .0612 BTC, and .0481 BTC, respectively.

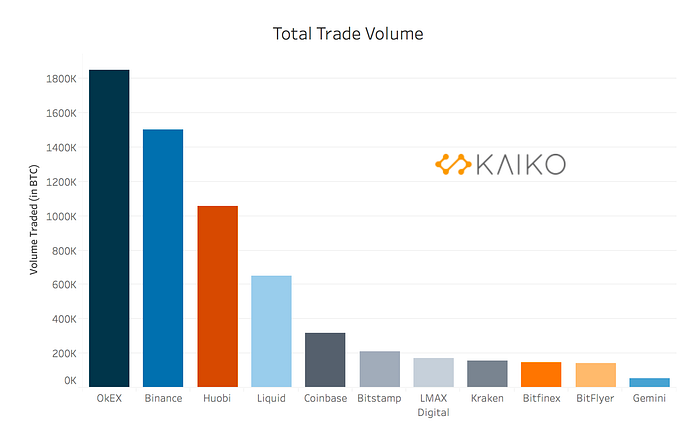

Next, we looked at the trade counts and trade volumes for the month of June, 2020.

Huobi takes the lead for trade count, at ~16 million trades recorded for the BTC-USDT pair. As expected, the exchanges with the lowest average trade size, Huobi, Binance, and Liquid, had some of the highest trade counts.

Trade volume revealed some interesting insights, in particular that of OKEx’s jump from 4th place in trade count to 1st place in trade volume. OKEx significantly outranks the 3 other retail-oriented exchanges in terms of trade volume. LMAX Digital also jumped from last in trade count to 7th in of trade volume, indicating trades are of a higher average value.

Interestingly, the top three exchanges in terms of volume offer trading for the BTC-USDT trading pair. BTC-USD exchanges, including Coinbase, Bitstamp, Kraken, Bitfinex, LMAX Digital and Gemini, had significantly lower overall trade volumes and counts.

Whale Trades

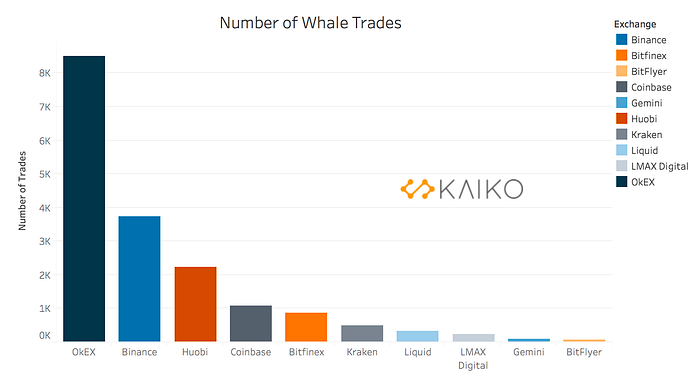

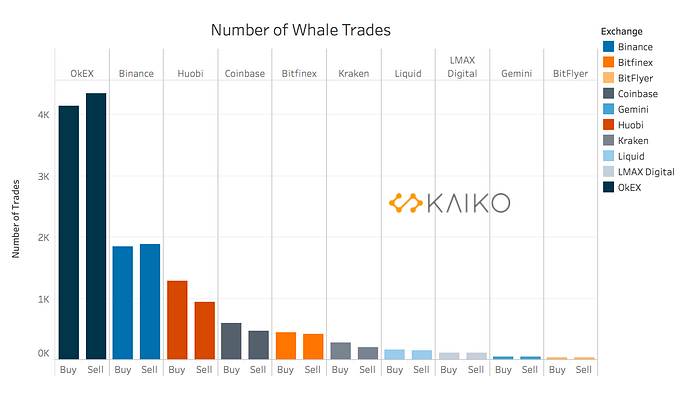

Now we will take a closer look at the composition of whale trades on these exchanges. We first look at the raw number of whale trades per exchange, which include all trades ≥ 10 BTC.

It is clear that OKEx, by and large, leads the pack in terms of the raw number of whale trades, clocking 8,500 trades ≥ 10 BTC in the month of June. While this chart does not reflect differences between exchanges in absolute trade count, we can compare it with the chart of total trade count to identify similarities and differences. OKEx, Binance, and Huobi remain in the top three exchanges, but we can observe that Liquid has fallen from fourth place in total trade count to eighth place in whale trade count, indicating that their user base skews retail.

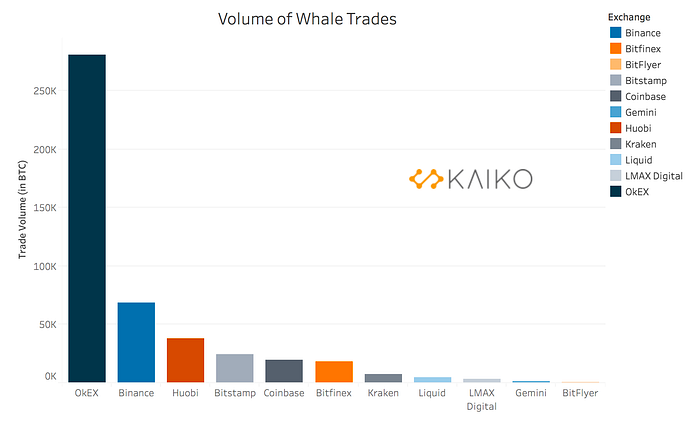

When we look at the volume of whale trades, we can observe that the exchange ranking stays the same, yet the whale trade volume on OkEX increases markedly compared with that of other exchanges.

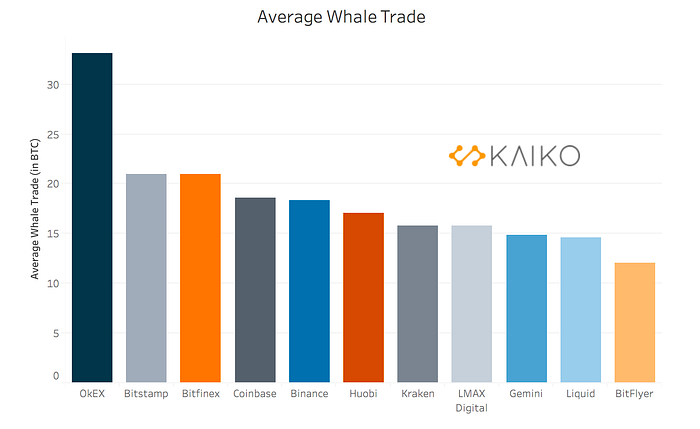

We next look at the average whale trade size, calculated by taking the average of all trades recorded at ≥ 10 BTC.

The exchange ranking for average whale trade size differs considerably compared with the ranking for average overall trade size, providing a more nuanced picture of an exchange’s user base.

Instead of LMAX Digital in first place, we again see OKEx leading all exchanges significantly, with an average whale trade size of 33.08 BTC. Both Kraken and LMAX Digital dropped from second and third place in average overall trade size to seventh and eighth place in average whale trade size.

It is clear that whale traders on OKEx place the largest trades. Those on Bitstamp and Bitfinex on average place trades just greater than 20 BTC. Liquid, Gemini, and BitFlyer did not have many whale trades in June, and when they did they were on average below 15 BTC.

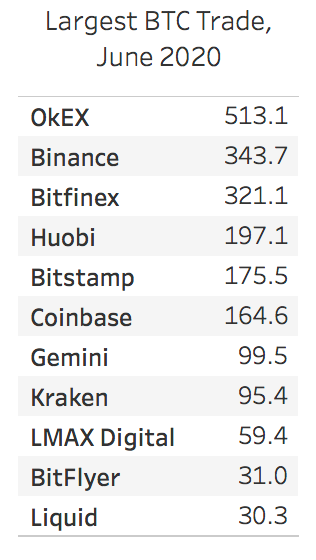

We then charted the top daily trade for the month of June.

We can observe that OKEx had the highest value trade every single day in June, ranging between 300 and 500 BTC. Below, we record the largest BTC trade made in the month of June on all 11 exchanges.

Buy vs. Sell Trades

We then charted trade count and volume with reference to the trade direction.

We can observe that when analyzing the raw number of buy vs. sell trades, there are not too many differences across exchanges. On Huobi, there were more buyers than sellers, and on OKEx, more sellers than buyers. Because the sample size of whale trades is a lot smaller than that of overall trades, the differences in buy vs. sell trade counts appear to be insignificant.

Yet, when we chart the volume traded of buyers vs. sellers, we notice that OKEx whale buy volume is nearly double that of OKEx sellers, despite OKEx sellers making more trades. The difference in buy vs. sell volumes across the other exchanges is similar to the differences in the count of trades.

Analysis

It is clear that OKEx leads the market in terms of whale trades, outranking all other exchanges in terms of average whale trade size, count, and volume. OKEx is one of the highest volume exchanges in the industry and plays a significant role in price discovery. In a report published in May 2020, MIT students found that OKEx is the leader in BTC price discovery, significantly outranking other exchanges like Coinbase, Bitstamp, and Liquid. This report further confirms that OKEx is important in cryptocurrency markets in their ability to attract high-volume traders.

In addition, this report shows that whale traders prefer high volume exchanges, which makes sense considering that liquidity is important to avoid price slippage for large trades. We do not analyze order book data, thus more research is needed to get a complete picture of exchange liquidity.

This report also shows that more whale trades are made on exchanges that support BTC-USDT compared with exchanges that support the BTC-USD pair.

Most surprising about this analysis is the fact that so many high-volume trades are made on a regular basis. Traders often opt to make high-volume trades over-the-counter to avoid the negative effects of price slippage. If an order book is not liquid enough to support a trade of, say, 100BTC, the price of the asset could fall significantly. Thus, it is quite promising to see that exchanges are able to regularly support trades of this size which indicates strong order book liquidity.

Finally, this report shows that the difference between “retail” and “institutional” exchanges is blurry at best. It is clear that retail exchanges have a significant user base of high-volume traders placing whale trades on a regular basis.

Conclusion

By analyzing trade count, size and direction, one can better understand the unique user bases of individual exchanges. The cryptocurrency exchange landscape is crowded, with hundreds operating around the globe competing for market dominance. In the next few years, we will likely see continued consolidation, but in the meantime exchanges must differentiate themselves in terms of the type of trader targeted and the trading features available, among other factors. These differences add up, resulting in unique user bases that can be better understood by analyzing trade data collected from these exchanges.

In Part 2, we will further explore the differences in exchange user bases by looking at buy/sell ratios and the distribution of trade volumes by category of trader.

[1] For example, Gemini writes on their website “Gemini is the leading crypto-native finance platform serving institutions. Our solutions meet the complex, high-stakes requirements of institutions without cutting corners on security, speed, or support.” whereas OKEx emphasizes their “global user base” and “high volumes.” Marketing language is important when classifying an exchange as retail vs. institutional. Most “institutional” exchanges have a visible section of their website dedicated to financial professionals, whereas more retail exchanges like Binance do not.

[2] Limitations: This report assumes that trade data collected from these exchanges represents actual trades made. Many exchanges will break apart a large trade into many small trades if the order book does not have enough volume to support the trade size. Some exchanges also allow iceberg orders, in which a trader can break apart a large order into smaller order sizes. However, iceberg orders on most exchanges can only be placed on an order book, and not executed as a market order. Thus, this would not affect trade data, which is normally recorded from the perspective of a “price taker.” Yet, every exchange has a slightly different methodology for recording trade data, often unspecified, which poses a limitation to fully understanding the extent of large trades made on these exchanges. We do not analyze order book data, thus more research is needed to get a complete picture of exchange liquidity.